How could the proposed 401(k) retirement policy affect housing demand?

January 23, 2026

Author: Roger Ashworth, Head of Research and Data

Prior to and at the World Economic Forum in Davos, the administration has hinted at a housing initiative that may allow households to access 401(k) assets for home purchases. While details remain limited and any tax-related changes would likely require legislative action, the concept raises a relevant question: to what extent could increased retirement savings liquidity translate into housing demand?

Balance Sheet Capacity Exists

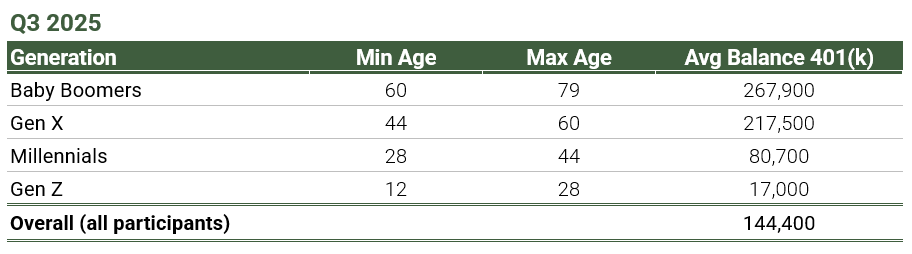

Data from major defined contribution plan providers indicate that households in prime homebuying years hold meaningful retirement assets. Fidelity reports average 401(k) balances for Millennials at approximately $80,000 as of Q3 2025, with median balances near $103,000 at year-end 2024 according to Vanguard. Given the strong equity market performance in 2025, balances are likely higher.

At the same time, the median existing home price remains near $400,000. A ~5% down payment (~$20,000)—consistent with FHA loan requirements—represents a relatively small fraction of reported retirement balances. From a balance sheet perspective, a subset of households appears capable of reallocating savings toward homeownership, assuming policy designreduces frictions such as early-withdrawal penalties.

Importantly, this would represent asset reallocation, converting tax-advantaged financial assets into housing equity.

Figure 1: 401(k) retirement balance by age group

Source: Vanguard Participant Plans, as of Q4 2024.

Source: National Association of Realtors, as of 2025.

Participation Is Likely the Binding Constraint

The macro impact hinges less on availability of funds and more on behavioral response. Standard financial guidance generally discourages the use of retirement assets for housing, citing opportunity costs and long-term retirement adequacy considerations.(1) Absent a meaningful tax incentive, participation rates may remain limited.

2024 Data indicated a rising rate of early withdrawals to 401(k) accounts. Vanguard, which tracks nearly five million defined contribution plan participants, shows that the share of participant staking a hardship withdrawal increased to approximately 4.8% in 2024, up from about 2% in the pre-pandemic period.

While hardship withdrawals reflect a range of uses and are not directly analogous to home purchases, the trend suggests that utilization of retirement assets is responsive to access rules and economic conditions. As a result, changes to withdrawal penalties or tax treatment could affect participation at the margin.

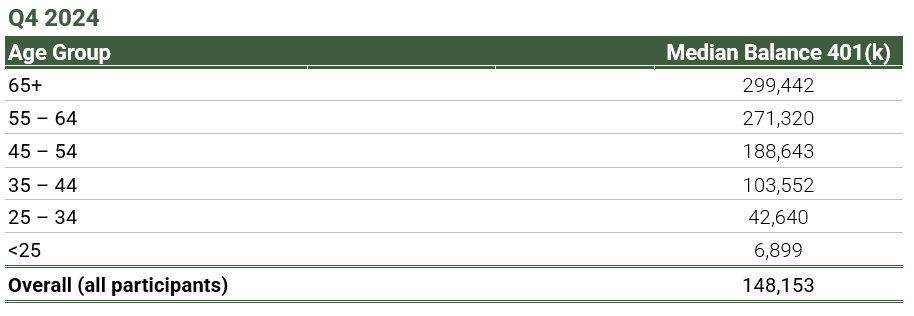

Figure 2: Median Existing Home Sales Price ($k)

Source: National Association of Realtors, as of 2025.

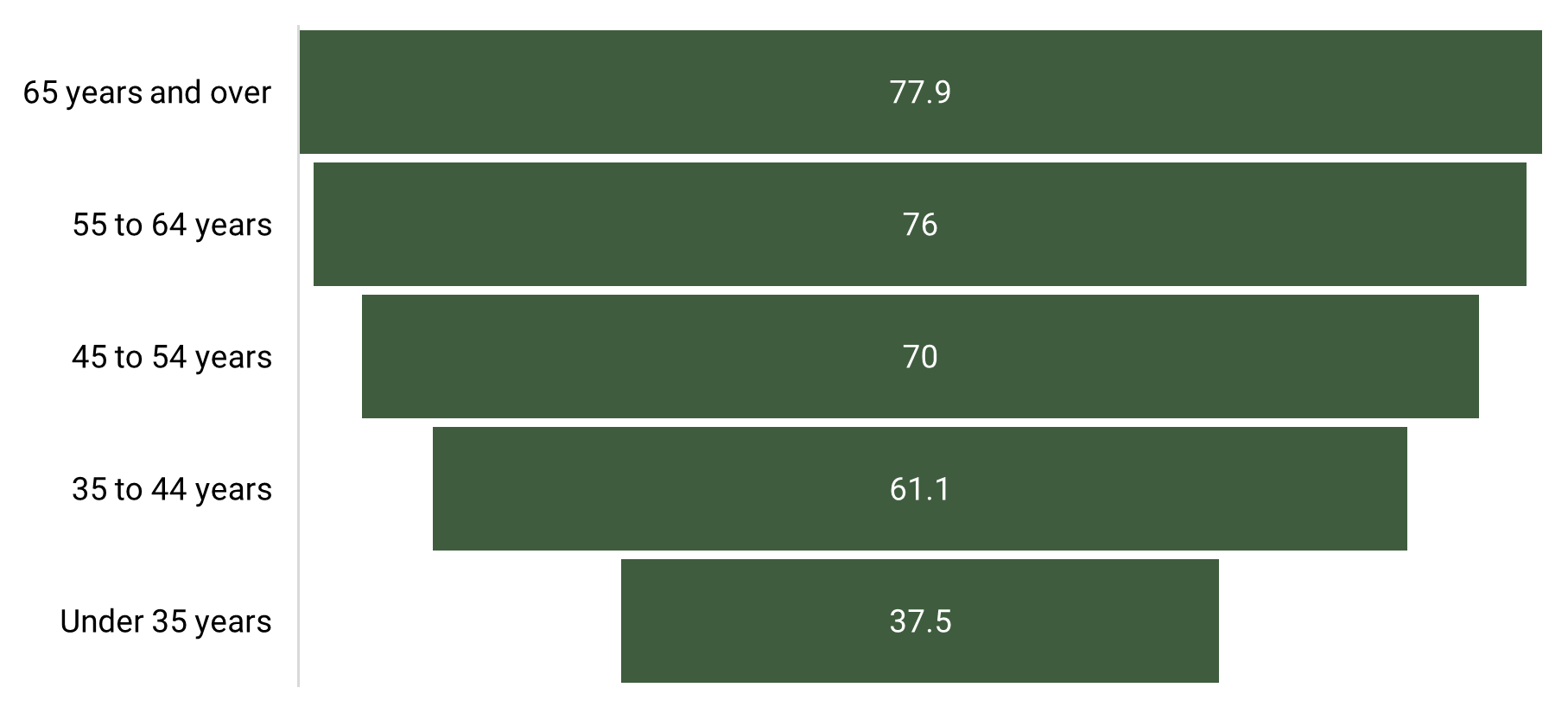

Figure 3: Home ownership rate by age group

Source: US Census, as of Q3 2025.

First-Time Buyer Incentives

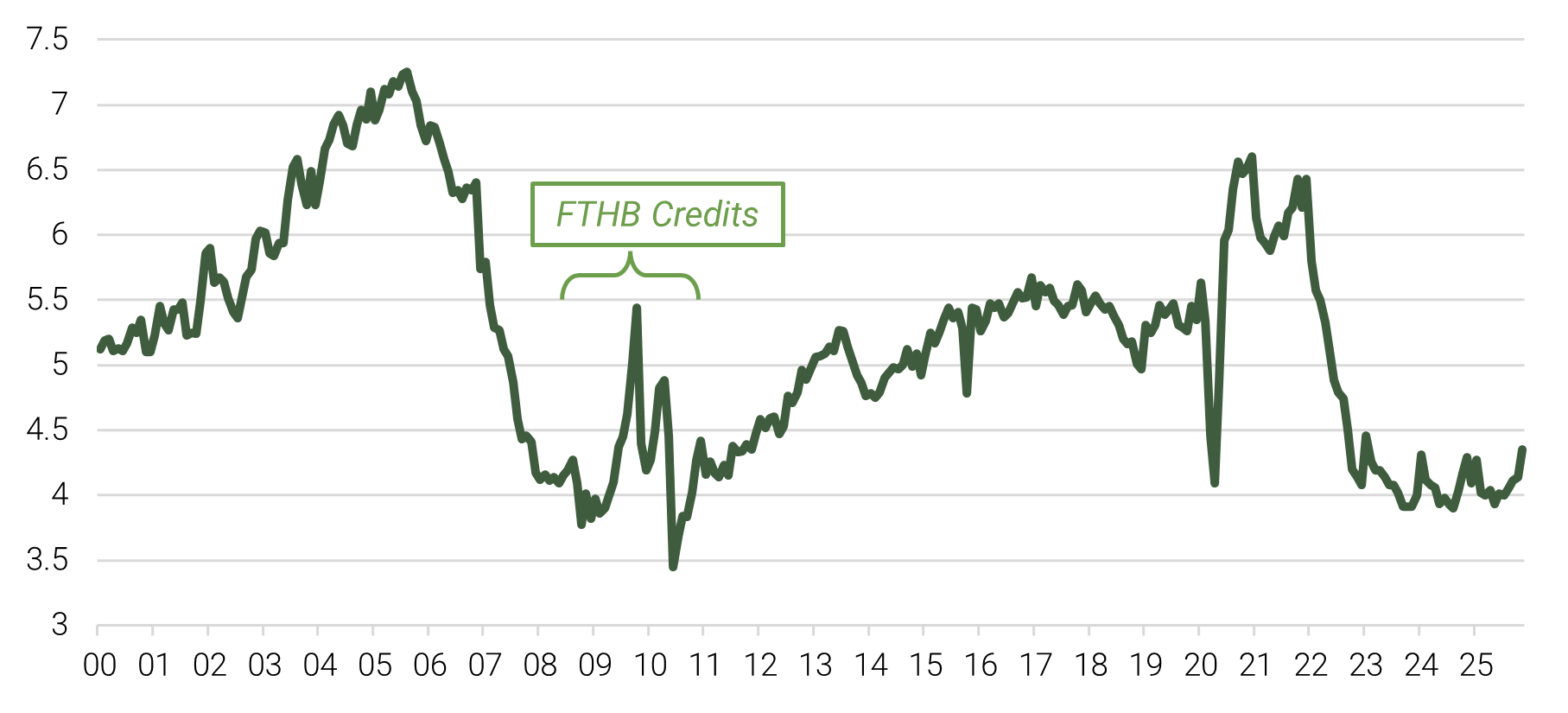

The closest precedent is the first-time homebuyer tax credit implemented between 2008 and 2010, where the federal government provided up to $8,000 per eligible buyer. Existing home sales increased during implementation periods, followed by a notable decline below trend once the program expired.

While today’s housing market differs meaningfully from the post-GFC environment—particularly with respect to credit availability and household balance sheet health—the historical pattern underscores a key macro consideration: housing incentives tend to alter timing more than long-run demand fundamentals.

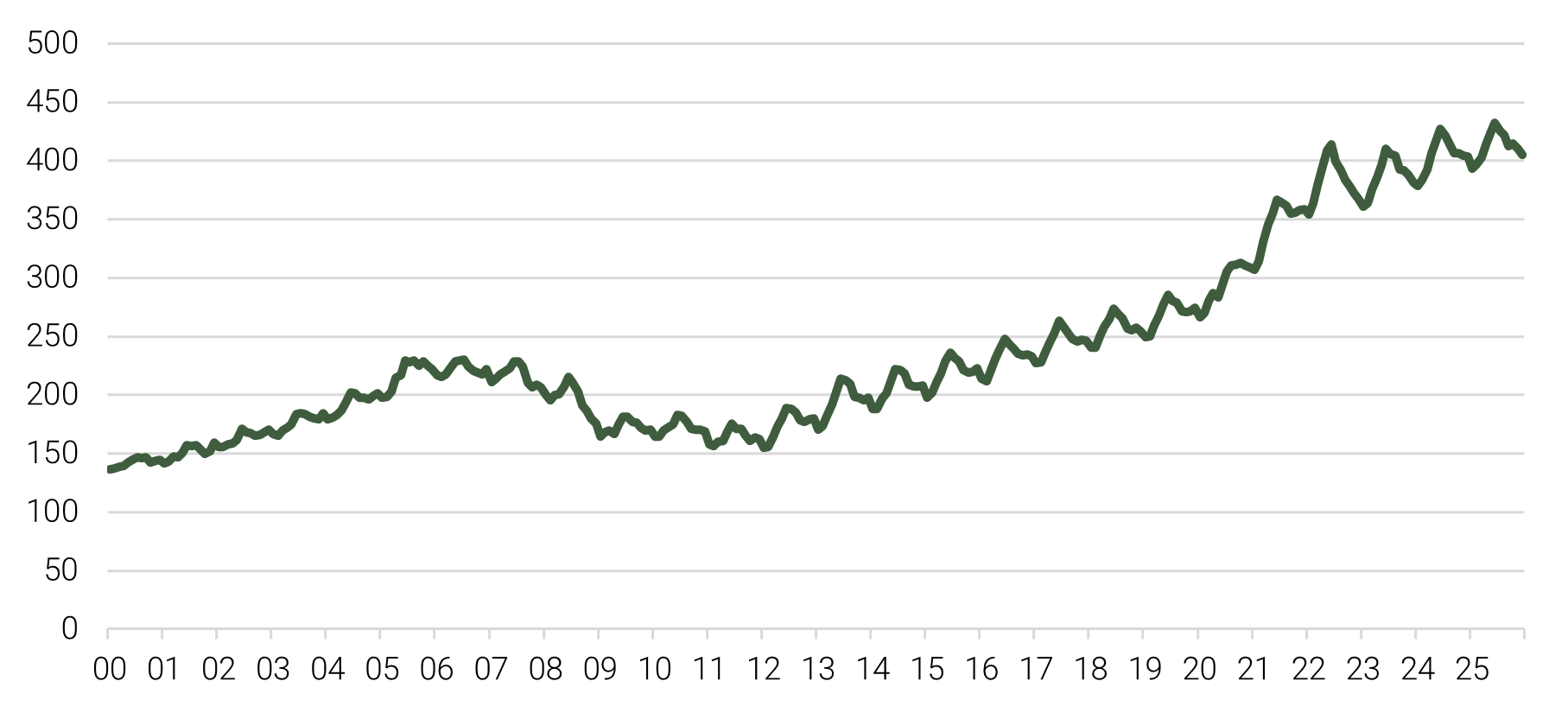

Figure 4: Existing home sales (SAAR #M)

Source: National Association of Realtors, as of 2025. FTHB = First Time Home Buyer.

Implications for Housing Markets

If enacted, expanded access to retirement assets could:

- Support a short-term increase in existing home sales, particularly at the entry-level and FHA-eligible segments

- Apply incremental price pressure, especially in supply-constrained regions

- Introduce intertemporal volatility in housing activity as demand is pulled forward

Takeaway

Whether the administration is willing to alter tax code treatment remains an open question, and execution details will matter. Even a narrowly tailored exemption could be enough to influence activity at the margin. While prevailing financial guidance generally discourages the use of retirement assets for housing, policy-driven changes in incentives could still shift household behavior.

Footnotes:

(1) Northwestern Mutual, Can you withdraw from your 401(k) to buy a house? Published June 4, 2025.

Disclaimer

These materials discuss general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. Recipients are urged to consult with their financial advisors before buying or selling any securities. The information included herein may not be current and Saluda Grade has no obligation to provide any updates or changes. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained herein. Certain information contained in these materials has been obtained from published and non-published sources prepared by third parties, which, in certain cases, have not been updated through the date hereof. While such information is believed to be reliable, Saluda Grade has not independently verified such information, nor does it assume any responsibility for the accuracy or completeness of such information. Except as otherwise indicated herein, the information, opinions and estimates provided in this presentation are based on matters and information as they exist as of the date these materials have been prepared and not as of any future date and will not be updated or otherwise revised to reflect information that is subsequently discovered or available, or for changes in circumstances occurring after the date hereof. Saluda Grade’s opinions and estimates constitute Saluda Grade’s judgment and should be regarded as indicative, preliminary and for illustrative purposes only. Certain information contained in this document constitutes forward-looking statements, and there is no representation or guarantee that they will occur.