Mid-Year Originator Pulse: What is the Market Signaling?

June 9, 2026

This commentary combines direct sentiment from Saluda Grade's mid-year outreach to originators, alongside our own market perspective. We attempt to distinguish between the two throughout. While the outreach was targeted and should not be read as a statistical survey, we believe the responses provide a representative view of current market conditions.

Why Originator Selection is Our Starting Point

Residential transition lending is highly execution dependent. Collateral condition, renovation progress, cost management, and exit timing are shaped by borrower quality and originator judgment. Many of these factors evolve between origination and exit, making active oversight of this asset class especially important.

We believe the strongest originators distinguish themselves through borrower sourcing, project-level diligence, ongoing construction monitoring, and the speed with which they respond when a loan moves off plan. For that reason, staying close to how these originators assess the market is an integral part of our risk underwriting and performance monitoring.

What Originators Are Telling Us

We recently posed a series of questions to our originator network as part of our ongoing market intelligence. The survey covered borrower quality, competitive pressure, underwriting discipline, and exit assumptions. Each question offered five possible answers, with respondents selecting one. Responses, therefore, reflect each originator's strongest priority at the time rather than the full scope of how they are managing their portfolios.

Responses were anonymous. To illustrate the types of questions asked, one example from the survey was: "How have your assumptions around borrower exit changed in the last 6 months?"

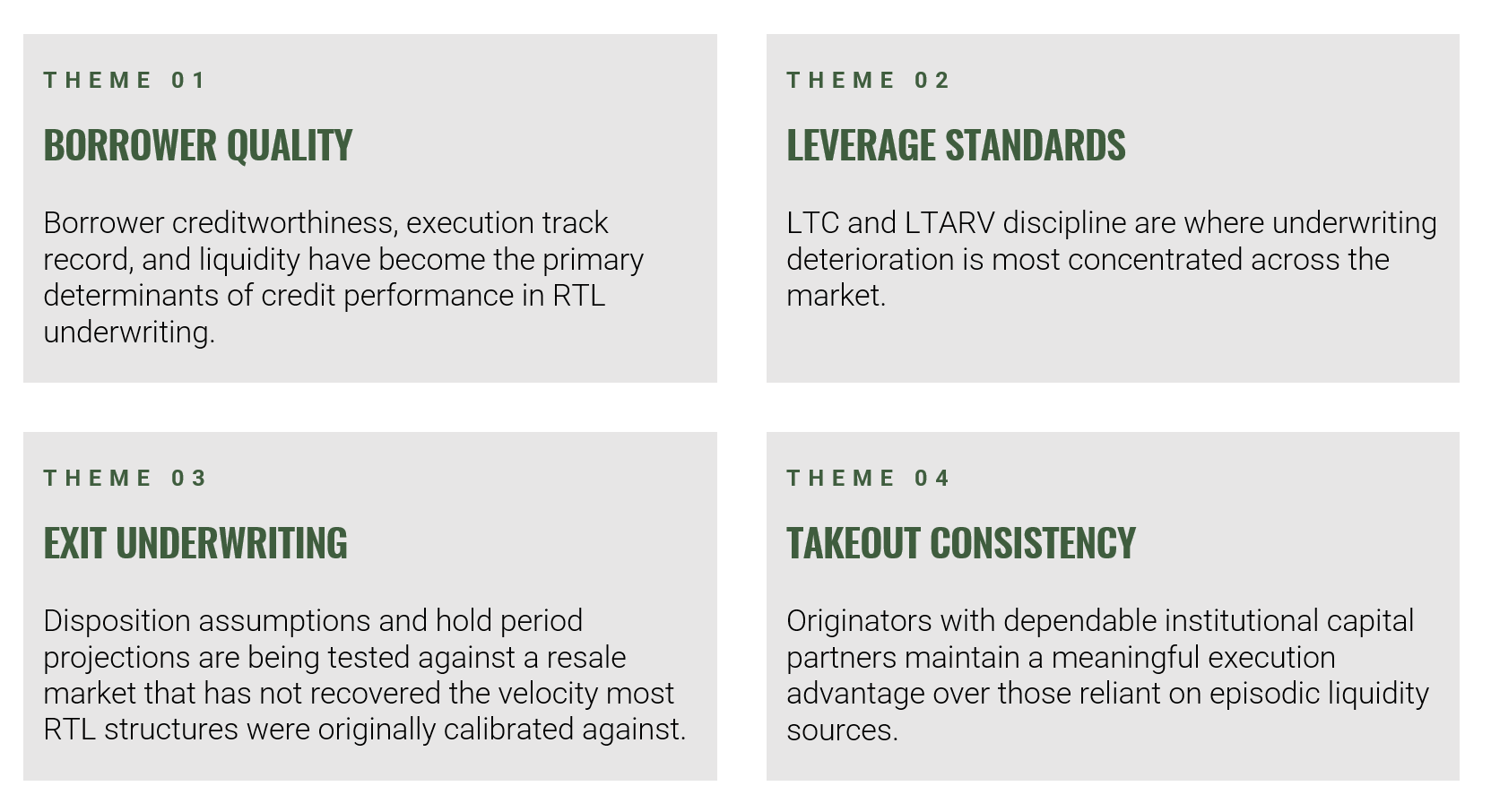

The goal was not to force consensus but to understand where experienced lenders aligned, where they differed, and what those patterns suggest about market risk. Four major themes emerged:

Saluda Grade's View

Originators are not describing a market where funding has disappeared. They are describing a market in which the harder question is whether available capital is being deployed with sufficient discipline. Proceeds friction, Loan-to-Cost (LTC) pressure, and weaker underwriting at the competitive margin are signs of a market where the terms required to win loans are increasingly difficult to defend under stress.

One signal deserves particular emphasis. Several originators noted that their credit selection approach is not a reaction to recent conditions. There is a meaningful difference between an originator that tightens under duress and one that never loosened its standards in the first place. We believe that difference is difficult to see in the current vintage but becomes much clearer when collateral takes longer to sell, extensions become more frequent, and the margin for error narrows.

On leverage, higher LTC or tighter spreads can be defensible for the right sponsor and the right project. The problem arises when the market stops making those distinctions. LTC and Loan-to-After-Repair-Value (LTARV) become expressions of loss severity, underwritten into a default resolution rather than competitive structuring terms. When credit standards compress broadly, losses accrue disproportionately where lenders extended furthest and assumed too much liquidity at exit.

The divergence in exit assumptions is the variable we are monitoring most carefully. The origination cycle of 2020 through 2022 produced structures calibrated to a disposition environment that no longer exists in many geographies. Some originators have already revised hold period and disposition assumptions based on observed portfolio seasoning. Others have not. That gap will not be apparent in current remittance data. We believe that the gap will not become measurable until the 2025 and 2026 loans mature. We hope that by asking these questions early on, we will be able to better assess whether our originator partners are applying appropriate exit underwriting before it appears in reported performance.

Takeout reliability is an extension of the same dynamic. Originators with consistent institutional capital partners can commit to sponsors with confidence in execution, manage warehouse dwell times more effectively, and sustain origination discipline through periods of market stress rather than contracting in response. Where episodic capital creates execution uncertainty at the loan level, the consistency of a capital partner becomes a credit variable in its own right.

Originators are not signaling a capital-constrained market. They are signaling a market where performance dispersion will be driven by credit selection, leverage discipline, and exit underwriting control. We believe the lenders best positioned through year-end will not simply be those willing to deploy capital. Origination volume is easiest to generate when capital is abundant and competitive pressure is high. They will be those with the rigor to identify which sponsors merit capital, which projects can support it, and which terms remain defensible if conditions deteriorate.

Disclaimer

These materials discuss general market activity, industry or sector trends, or other broad-based economic, market, or political conditions and should not be construed as research or investment advice. Recipients are urged to consult with their financial advisors before buying or selling any securities. The information included herein may not be current and Saluda Grade has no obligation to provide any updates or changes. No representation, warranty, or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained herein. Certain information contained in these materials has been obtained from published and non-published sources prepared by third parties, which, in certain cases, have not been updated through the date hereof. While such information is believed to be reliable, Saluda Grade has not independently verified such information, nor does it assume any responsibility for the accuracy or completeness of such information. Except as otherwise indicated herein, the information, opinions and estimates provided in this presentation are based on matters and information as they exist as of the date these materials have been prepared and not as of any future date and will not be updated or otherwise revised to reflect information that is subsequently discovered or available, or for changes in circumstances occurring after the date hereof. Saluda Grade’s opinions and estimates constitute Saluda Grade’s judgment and should be regarded as indicative, preliminary and for illustrative purposes only. Certain information contained in this document constitutes forward-looking statements, and there is no representation or guarantee that they will occur. Certain statements contained herein may be deemed testimonials or endorsements. Such statements may have been provided by current clients, former clients, or non-clients. No compensation, cash or non-cash, was provided in exchange for these statements. Any testimonial or endorsement reflects the individual’s personal experience and opinion, which may not be representative of the experience of all clients. There is no guarantee that any client or investor will have a similar experience or achieve similar results. The firm does not believe that any testimonial or endorsement presented herein creates a material conflict of interest. However, prospective clients should consider that such statements may not be indicative of future performance or success and should not be relied upon as the sole basis for an investment decision.