What is the net impact of tariffs on residential construction costs now?

February 25, 2026

Author: Roger Ashworth, Head of Research and Data

On February 20, 2026, the Supreme Court ruled in Learning Resources, Inc., et al. v. Trump, President of the United States, et al., 607 U.S. (Feb. 20, 2026) (No. 24-1287) that the International Emergency Economic Powers Act (IEEPA) does not authorize the President to impose tariffs. The decision immediately eliminated a significant portion of the Trump administration’s 2025 tariff expansion.

For residential construction, however, the relevant question is not legal authority but cost: how much tariff-driven pressure on homebuilding remains?

Our analysis suggests tariff-related construction cost inflation has declined from a peak of roughly 7–8% of construction costs in mid-2025 to approximately 4–5% today — or from roughly $17,000–$22,000 per home to approximately $8,000–$12,000. The reduction is material. But the remaining exposure is now more concentrated in structural materials, particularly lumber, steel, and aluminum, where tariffs remain in force under other statutory authorities.

Background: The SCOTUS ruling and its scope

In a 6-3 decision, the Supreme Court ruled that the International Emergency Economic Powers Act (IEEPA) does not authorize the President to impose tariffs. Because IEEPA had been used to implement broad “reciprocal” tariffs across many trading partners, the ruling eliminated a significant layer of duties added in 2025. IEEPA tariffs accounted for an estimated $130–175 billion, roughly half of total tariff revenue last year.

However, the ruling did not affect tariffs imposed under other statutory authorities. The following remain in force:

- Section 232 tariffs (national security) on steel, aluminum, copper, lumber, and timber

- Antidumping, or imports sold at below fair value, and countervailing duties, or recovery of subsidy received by foreign governments for subsidized imports (AD/CVD), on Canadian softwood lumber

- Section 301 tariffs on Chinese goods

Within hours of the ruling, the administration invoked Section 122 of the Trade Act of 1974 imposing a temporary 10% global tariff (later raised to 15%) on non-exempt goods. This tariff is limited to 150 days and requires Congressional approval for extension.

Construction cost structure and tariff exposure

According to the National Association of Home Builders' (NAHB) 2024 Cost of Construction Survey, the average construction cost of a new single-family home is approximately$428,215, representing 64.4% of the average sale price of $665,298 — a record high. Understanding how tariffs affect each material category requires analysis at two levels: (1) the share of construction cost attributable to each category, and (2) the degree of import exposure within each category.

Tariff exposure ultimately depends on four interacting variables:

- A material’s share of construction cost

- The share of U.S. supply that is imported

- The effective tariff rate

- The degree of pass-through into final pricing

While actual pass-through may vary by region and supply chain flexibility, this framework provides a directional estimate of exposure.

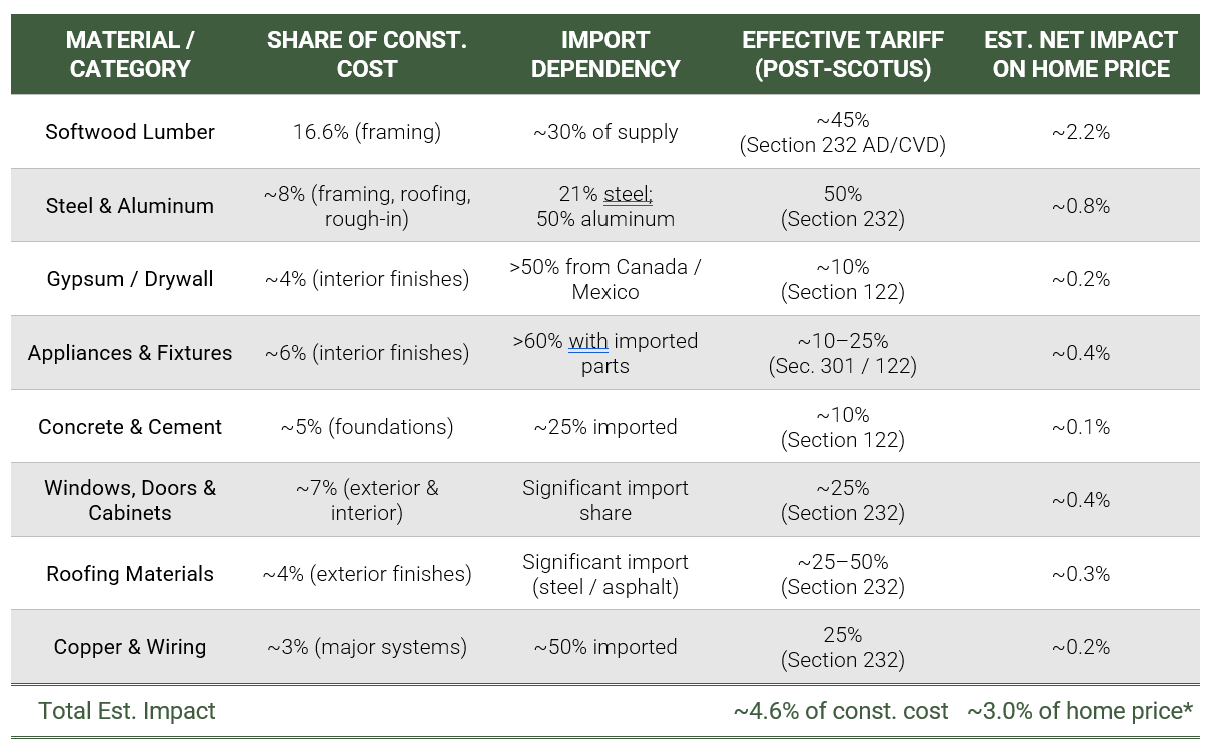

Figure 1: Building material impact analysis (Post-SCOTUS ruling, February 2026)

Source: Construction cost shares based on NAHB 2024 Cost of Construction Survey. Import shares based on NAHB, Congressional Research Service, and Brookings Institution data. Tariff rates reflect post-ruling regime effective as of February 21, 2026.

*Net impact calculation: (import share) × (effective tariff rate) × (material share of construction cost) × (64.4% construction cost share of home price). Assumes full pass-through. Actual impact may be lower due to domestic substitution, margin compression, and pass-through rates. The $10,900 per-home estimate from NAHB's April 2025 builder survey (~1.6% of average home price) serves as an independent cross-check.

Lumber: The most significant structural exposure

Lumber appears to remain the most consequential tariff exposure for residential construction. The U.S. imports ~40% of its softwood lumber, with Canada accounting for over 80% of that volume. This means that Canadian lumber represents approximately 30% of total U.S. supply.

Framing, which relies heavily on softwood lumber, accounts for 16.6% of construction costs, making it one of the largest single cost categories in a new home. The effective tariff rate on Canadian lumber is currently estimated at ~45%, combining longstanding AD/CVD duties (~14.5%) with Section 232 tariffs imposed in late 2025. Neither of those measures was implemented under IEEPA. As a result, the Supreme Court’s invalidation of IEEPA tariffs did not materially change the effective duty on Canadian lumber. While the broader 2025 tariff environment included IEEPA-based actions, the core lumber duties were anchored in separate statutory authorities and therefore remain intact.

Applying NAHB’s cost shares as a guide, lumber alone may account for ~1.4% of total home price, well above the 1% figure commonly cited using the 25% supply assumption.

Other materials: Continued exposure under Section 232

Relief is more visible in categories where IEEPA is layered on top of other authorities.

Gypsum (drywall) and concrete present moderate exposure. Over 50% of gypsum imports come from Canada and Mexico; these were subject to IEEPA tariffs that have now been eliminated. However, the new 15% Section 122 tariff creates a partial replacement. Concrete is largely domestically produced, but imported additives, cement clinker, and specialized equipment face tariff pressure. Together, these materials contribute a modest but real cost increment.

Appliances and certain fixtures present mixed exposure depending on sourcing. Over 60% of major appliances contain imported parts or assemblies. Chinese-sourced goods remain subject to Section 301 tariffs ranging from 25% to 145%, which the SCOTUS ruling did not touch. The IEEPA tariff component affecting other import origins has been removed. The net result is partial relief for this category.

Post-SCOTUS regime: What changed and what remains

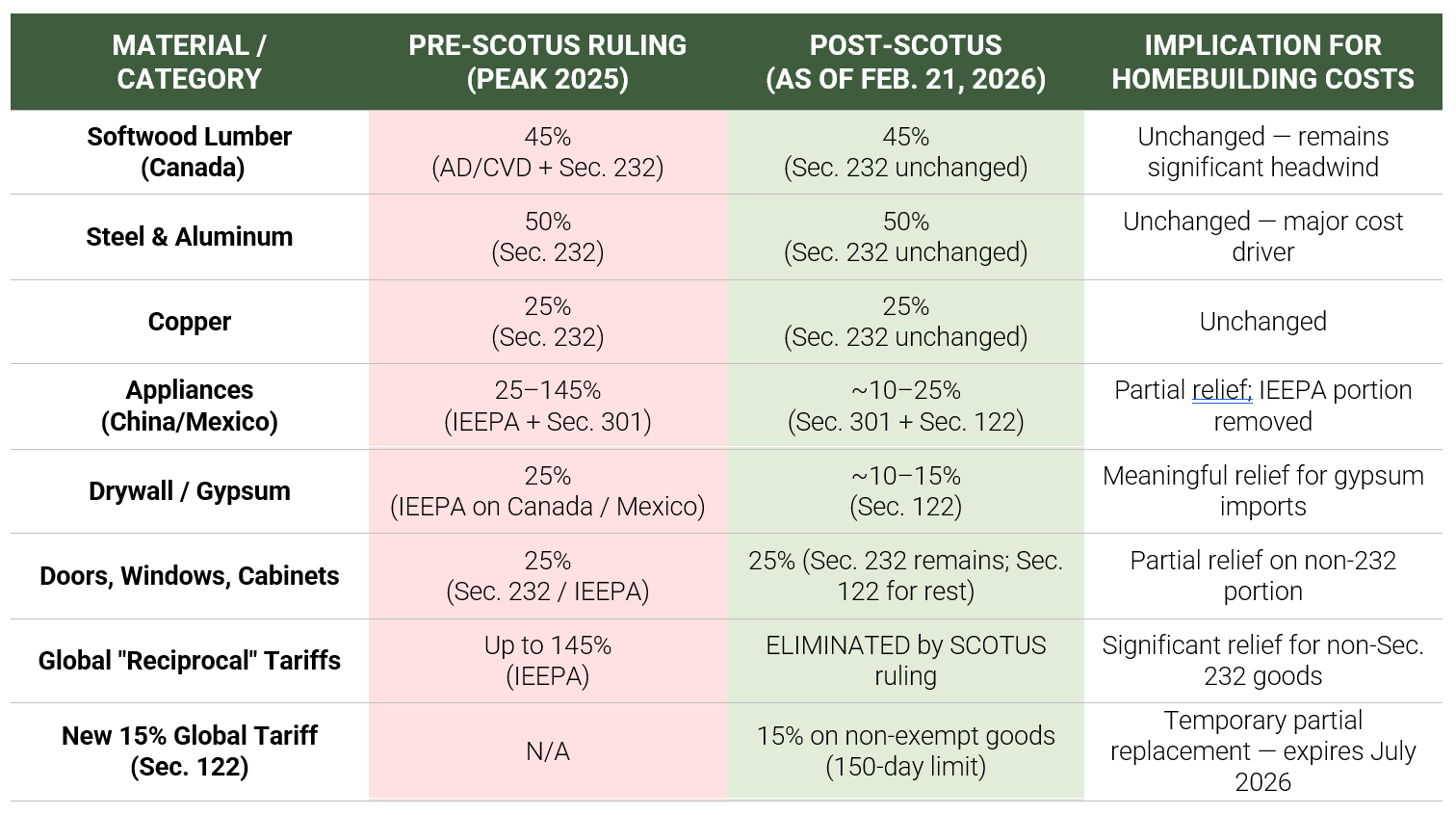

Figure 2: Building material tariff regime - before and after Supreme Court ruling

Source: WilmerHale, Brownstein, Global Trade Alert, Tax Foundation.

*Red cells indicate tariff regimes that remain elevated. Green cells indicate relief for elimination. The 15% Section 122 global tariff is explicitly temporary (150-day limit, expires ~July 2026) and excludes USMCA-compliant goods from Canada and Mexico. Congress would need to authorize an extension.

Net-impact: Peak 2025 vs. today

Based on our analysis and corroborated by NAHB survey data, builder earnings disclosures (D.R. Horton, Lennar), and third-party research from Brookings and the Tax Foundation, the net tariff impact on a typical new single-family home can be summarized as follows:

Mid-2025 (Peak Impact):

- Estimated $17,000–$22,000 per home, or approximately 2.6–3.3% of the average home price

- Equivalent to construction cost increases of 7–9%.

February 2026 Revision (Post-SCOTUS):

- Estimated $8,000–$12,000 per home, or roughly 1.2–1.8% of home price

- Equivalent to ~4–5% of construciton costs

Our bottom-up material analysis yields approximately $12,800 per home (~3% of home price) assuming full pass-through, broadly consistent with NAHB’s April 2025 builder survey estimate of $10,900.

In practical terms, the ruling appears to have removed roughly half of peak tariff-driven cost inflation but left intact the portion tied to structural materials.

Conclusion

The broad tariff overlay imposed in 2025 has been materially reduced. Categories such as gypsum, appliances, and certain interior goods will likely see measurable relief following the elimination of IEEPA-based duties.

However, the tariffs most relevant to structural residential construction — softwood lumber (AD/CVD and Section 232), steel, aluminum, and copper (Section 232) — remain in place. These inputs account for a disproportionate share of base construction costs and are less easily substituted.

Residential construction is no longer facing a generalized tariff shock, but it is still operating with an embedded 4–5% structural cost headwind concentrated in core materials.

For builders, lenders, and residential credit investors, this does not represent a return to pre-2025 cost conditions. It represents a shift from peak policy-driven inflation to a more persistent, structurally elevated cost baseline.

Sources

- National Association of Home Builders (NAHB), "2024 Cost of Construction Survey and Tariff Impact Analyses."

- Congressional Research Service (R48781), "U.S.-Canada Softwood Lumber Trade."

- Brookings Institution, "Recent Tariffs Threaten Residential Construction," Oct. 2025.

- WilmerHale, "SCOTUS IEEPA Tariff Ruling Alert," Feb. 2026.

- Tax Foundation, "Supreme Court IEEPA Ruling Analysis," Feb. 2026.

- Global Trade Alert, "Post-SCOTUS Tariff Impact Analysis," Feb. 2026.

- HBS Dealer, "Weighing the Downstream Impact of Tariffs on Canadian Lumber," Oct. 2025.

- D.R. Horton Q3 2025 Earnings Call.

- Center for American Progress housing analysis, Dec. 2025.

Disclaimer

These materials discuss general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. Recipients are urged to consult with their financial advisors before buying or selling any securities. The information included herein may not be current and Saluda Grade has no obligation to provide any updates or changes. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained herein. Certain information contained in these materials has been obtained from published and non-published sources prepared by third parties, which, in certain cases, have not been updated through the date hereof. While such information is believed to be reliable, Saluda Grade has not independently verified such information, nor does it assume any responsibility for the accuracy or completeness of such information. Except as otherwise indicated herein, the information, opinions and estimates provided in this presentation are based on matters and information as they exist as of the date these materials have been prepared and not as of any future date and will not be updated or otherwise revised to reflect information that is subsequently discovered or available, or for changes in circumstances occurring after the date hereof. Saluda Grade’s opinions and estimates constitute Saluda Grade’s judgment and should be regarded as indicative, preliminary and for illustrative purposes only. Certain information contained in this document constitutes forward-looking statements, and there is no representation or guarantee that they will occur.