Will capital relief reopen the second lien market for banks?

February 27, 2026

Author: Roger Ashworth, Head of Research and Data

Federal Reserve Vice Chair for Supervision Michelle Bowman(1) has outlined a proposal to “revitalize” bank participation in mortgage origination and servicing. The two pillars of her proposal are:

- Mortgage servicing rights (MSRs): eliminating the requirement to deduct MSRs from regulatory capital while retaining a 250% risk weight.

- Portfolio mortgages: proposing more risk-sensitive capital treatment for first lien mortgages, potentially tiered by loan-to-value (LTV), rather than a uniform 50% risk weight.

The framing is revitalization. The more precise question is: If capital treatment becomes more granular for first liens, does that meaningfully change the economics of junior liens — particularly second lien mortgages?

Our base case is that it does not.

What changes? And what does not?

We believe Bowman’s argument is that current capital rules may be insufficiently risk-sensitive, particularly for low-LTV, first lien mortgages. Under today’s standardized capital approach:

- Qualifying first liens receive a 50% risk weight

- Junior liens receive a 100% risk weight

Bowman has indicated support for a more granular approach, conceptually similar to original Basel III standards, where low-LTV first liens could carry meaningfully lower capital requirements, potentially in the 20-30% range.(2)

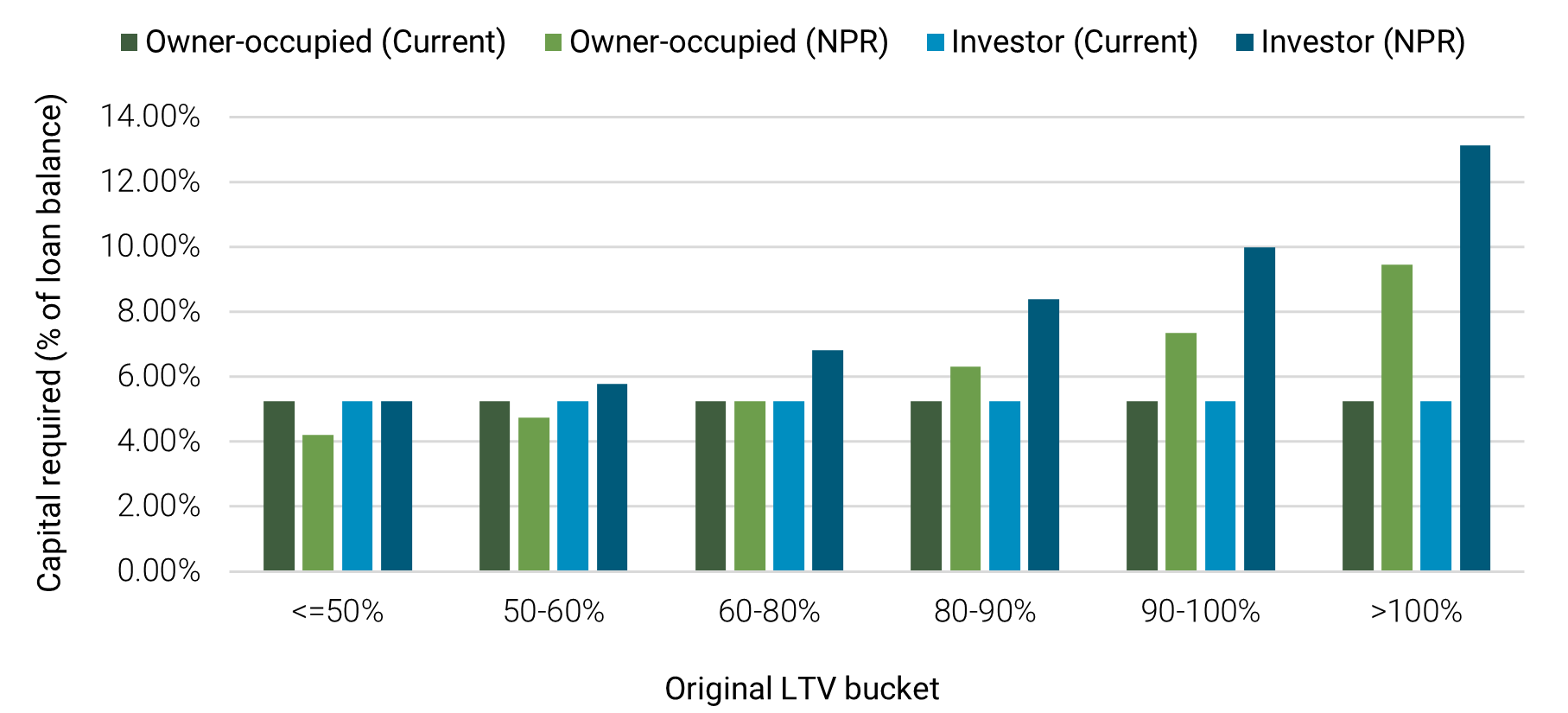

Figure 1: Capital required rises with LTV in the proposed framework

Source: Urban Institute summary of the U.S. Basel III endgame NPR (risk weights) with an illustrative 10.5% total capital assumption.

Assuming a ~10.5% total capital requirement (inclusive of buffers), capital held against a mortgage exposure equals:

Risk Weight * 10.5%

Under a granular structure:

- A 50% risk weight implies ~5.3% capital against the loan balance

- A 30% risk weight implies ~3.2% capital

The effect is straightforward: Low-LTV first liens become materially more capital-efficient, while higher-LTV exposures require progressively more capital. The capital curve becomes steeper — more sensitive to LTV.

What does not change is lien treatment. There is no indication that junior liens would receive LTV-sensitive risk weights. Under current standardized rules, they carry a 100% risk weight — regardless of LTV, or other credit metrics.

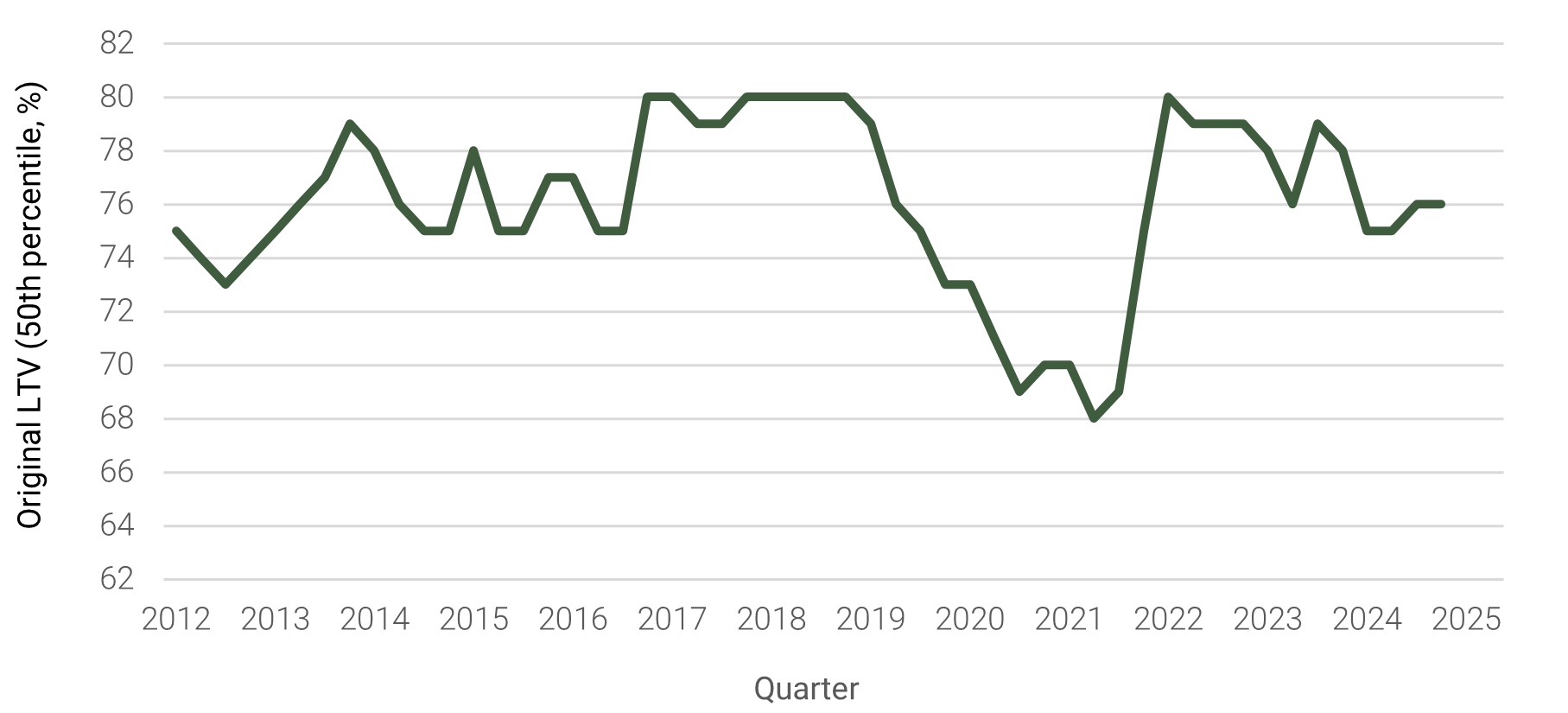

Relief aligns with where banks already concentrate

Large-bank portfolio data show that retained first lien mortgages are concentrated in lower-LTV exposures.(1) Approximately:

- 50% of outstanding balances were originated at ≤72% LTV

- 75% at ≤80% LTV

Figure 2: Large-bank portfolio mortgage originations - median original LTV

Source: Federal Reserve Bank of St. Louis (FRED), FR Y-14M Large Bank Credit Card and Mortgage Data, “Large Bank Consumer Mortgage Originations: Original LTV (50th percentile).”

Median original LTV for large-bank portfolio originations has generally remained in the mid-70% range, with limited sustained movement higher. The primary beneficiaries of risk-weight relief are exposures banks already originate and retain.

A recent Morgan Stanley(1) estimate suggests that if ~$2.2 trillion of mortgages currently in the 50% risk-weight bucket stepped down to 30-40%, banks could free up $30-70 billion of capital or support $0.5-1.4 trillion of incremental mortgage capacity.

That is meaningful balance sheet capacity. But capacity expansion does not imply expansion across lien positions.

Why second liens remain structrally capital-heavy

The capital asymmetry becomes clearer when examining junior liens.

Under today’s standardized capital rules:

- First lien → 50% risk weight

- Junior liens → 100% risk weight

At a 10.5% capital requirement:

- 50% risk weight → ~5.3% capital against the loan balance

- 100% risk weight → ~10.5% capital against the loan balance

A second lien therefore requires roughly double the capital of a qualifying first lien.

Importantly, this differential is driven by lien position – not borrower credit quality.

A low-LTV, high-FICO second lien still receives a 100% risk weight. By contrast, under Bowman’s proposed framework, a comparable first lien would likely receive materially lower treatment as LTV declines.

The asymmetry is structural: capital treatment improves with LTV for first liens but remains fixed for junior liens.

From a bank return-on-equity perspective, capital freed from low-LTV first liens is more efficiently redeployed into additional first liens than into seconds carrying double the capital charge.

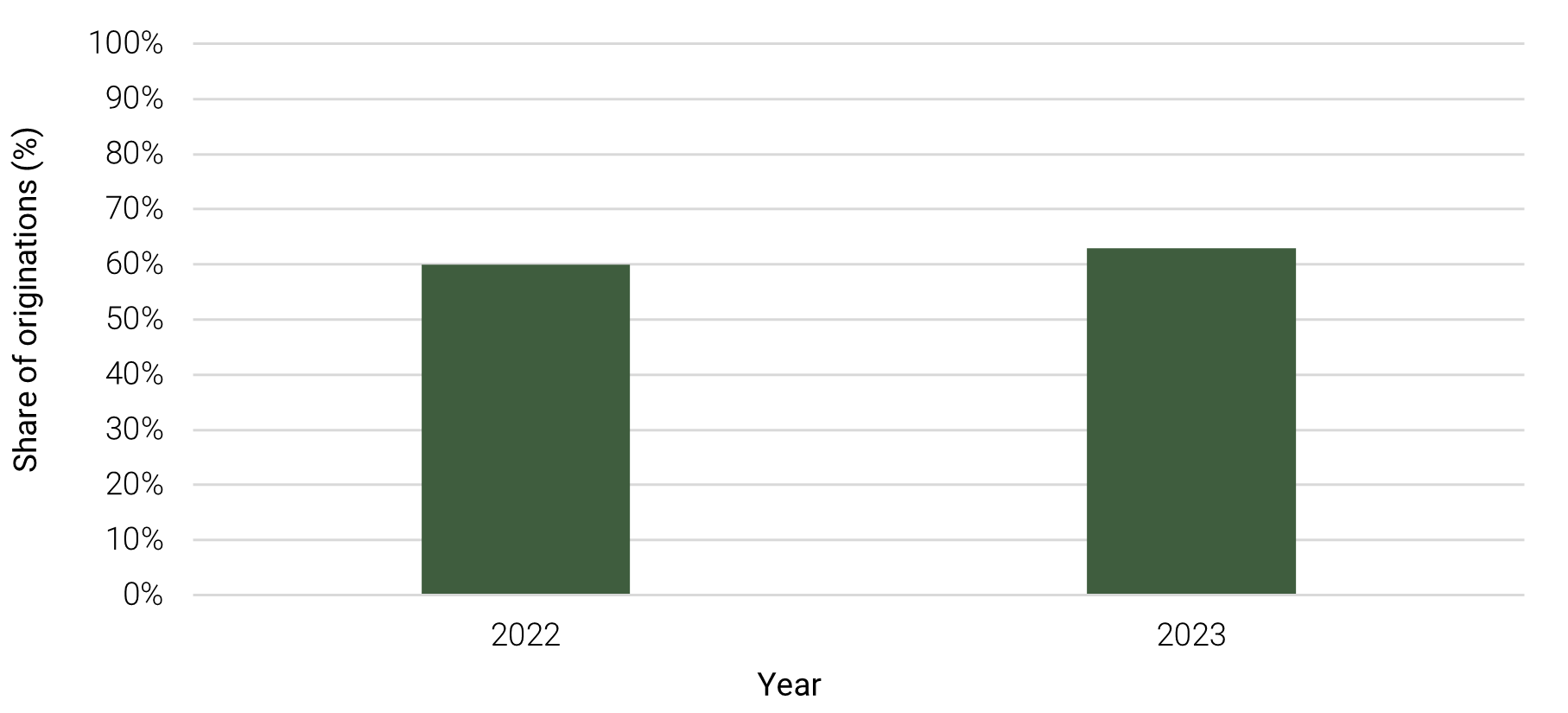

The structural shift toward non-banks

Mortgage origination has moved decisively toward non-banks over the past decade. Independent mortgage companies now account for roughly 70% of total originations, and their share of first lien home-purchase loans increased from 60% in 2022 to 63% in 2023.

Figure 3: Independent mortgage companies' share of first lien home-purchase originations

Source: FFIEC/CFPB announcement on 2023 HMDA mortgage lending data.

Additionally, banks’ share of agency originations among the largest lenders stands at just 11%.(3)

This migration was not solely the result of capital treatment. It reflected:

- Post-crisis litigation exposure

- Higher compliance and liquidity requirements

- Business model reprioritization

- Technological scale advantages at non-banks

The proposal addresses one constraint — the capital treatment of low-risk first liens and MSRs. It does not alter the structural cost, compliance, and business model asymmetries that drove non-bank share gains.

Reversing the structural evolution of the market would require parity across these dimensions — not incremental relief targeted at prime first liens.

What "revitalization" likely means

If implemented, Bowman’s proposal should improve capital efficiency for low-LTV first liens and increase the attractiveness of retaining both mortgages and servicing.

Banks may hold more prime mortgages on balance sheet as risk weights decline for safer exposures. MSR economics may also improve at the margin.

What appears less likely is a broad pivot into second liens.

Even where borrower credit quality and combined LTV are comparable, junior liens continue to carry roughly double the capital charge of first liens.

Absent parity in lien treatment, “revitalization” most plausibly means reinforcement — not expansion.

Sources

- Michelle W. Bowman (Feb. 16, 2026), “Revitalizing Bank Mortgage Lending, One Step with Basel.”

- Morgan Stanley, “Bowman Confirms Two New Bank Mortgage Proposals on the Way,” Published February 2026.

- Saluda Grade analysis of the 2023 HMDA Mortgage Lending Data.

Disclaimer

These materials discuss general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. Recipients are urged to consult with their financial advisors before buying or selling any securities. The information included herein may not be current and Saluda Grade has no obligation to provide any updates or changes. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained herein. Certain information contained in these materials has been obtained from published and non-published sources prepared by third parties, which, in certain cases, have not been updated through the date hereof. While such information is believed to be reliable, Saluda Grade has not independently verified such information, nor does it assume any responsibility for the accuracy or completeness of such information. Except as otherwise indicated herein, the information, opinions and estimates provided in this presentation are based on matters and information as they exist as of the date these materials have been prepared and not as of any future date and will not be updated or otherwise revised to reflect information that is subsequently discovered or available, or for changes in circumstances occurring after the date hereof. Saluda Grade’s opinions and estimates constitute Saluda Grade’s judgment and should be regarded as indicative, preliminary and for illustrative purposes only. Certain information contained in this document constitutes forward-looking statements, and there is no representation or guarantee that they will occur.